Commercial Auto insurers face an environment of continuing challenges

ArticleAugust 11, 2021

by Alex Wells, Head of U.S. Middle Market, Zurich North America

This article is part of a four-part series, focusing on the current and historical trends for various commercial insurance products. Other articles will focus on Workers’ Compensation, General Liability and Property.

Trends in Commercial Insurance, Issue 1 of 4: Auto

For midsize businesses, maintaining an effective, comprehensive commercial insurance program is a first line of defense against risks that can severely threaten an insured’s financial stability. And one of the most important components of any midsize client’s insurance program is Commercial Automobile coverage. This line of insurance protects the company against the financial consequences of accidents, injuries and fatalities involving company-owned or leased vehicles as well as employees’ vehicles when used on business.

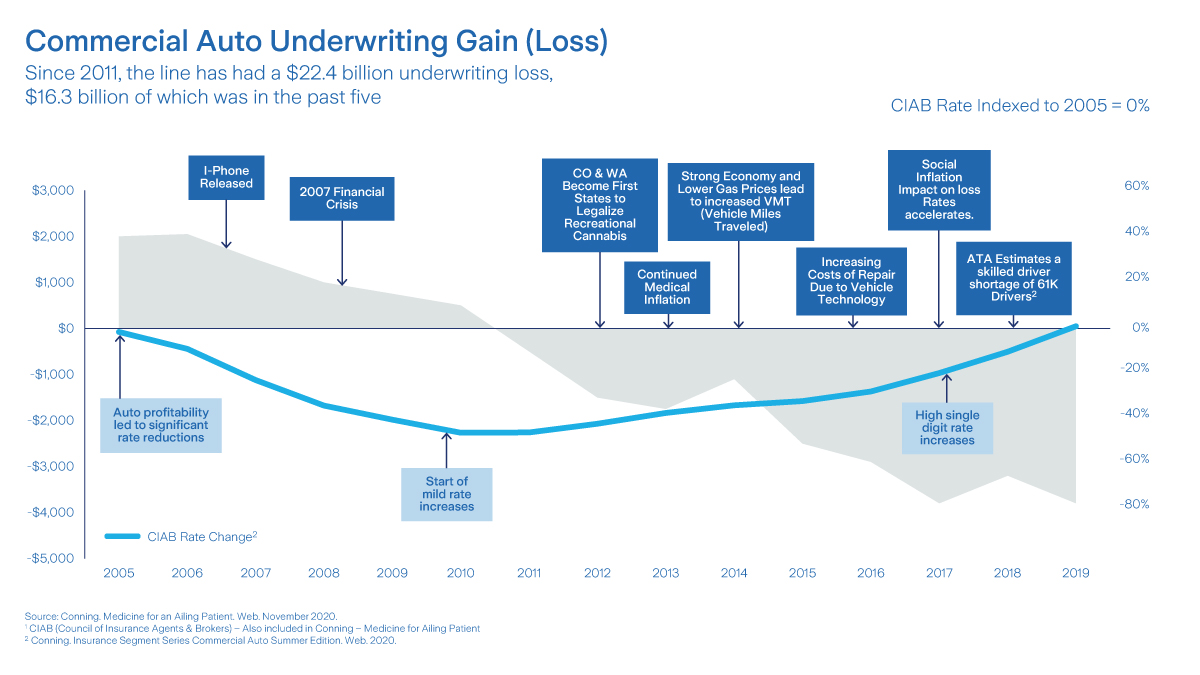

For the better part of a decade, the Commercial Auto line has been affected by a confluence of factors that have severely impacted insurers’ profitability. A recent Conning, Inc. report noted that the industry’s Commercial Auto combined ratio has averaged a troubling 107 since 2010. The same report states that from 2011 to 2019, Commercial Auto has accounted for $22.4 billion in underwriting losses for the industry, $16.3 billion of which came from just the last five years of that report (2015-2019).1

Looking back, from 2005 to 2010, the Auto line was profitable, with 2011 becoming a turning point in terms of profitability. What changed? Simply, a variety of adverse loss trends have intensified significantly, joined by others that did not exist in their present form in years past.

Smartphones – While cellphones have been a fixture of American life since the 1990s, the introduction of the first iPhone in 2007 represented a sea change. The modern smartphone propelled the risks of distracted driving to a whole new level. According to the Insurance Institute for Highway Safety (IIHS), based on national police-reported data on fatal crashes in the United States during 2019, 3,142 people died in motor vehicle crashes in which distraction was deemed a contributing factor. That is nearly 9% of all crash deaths.2

Not all distracted driving accidents involved smartphones, but the challenge is growing. Data suggests that even the use of hands-free devices while driving is contributing to distracted driving accidents.

Legal cannabis – As more states decriminalize and legalize medical and recreational use of cannabis, a new dimension of impaired driving has entered the picture. According to the IIHS, crash rates have indeed increased with the legalization of cannabis across the U.S.3

While there are a variety of time-tested tools and techniques police officers have used to discern impairment due to alcohol, there exist no truly reliable tests to measure the level of impairment a driver may have after using cannabis products. According to data from the National Highway Transportation Safety Administration (NHTSA), the percentage of fatally injured drivers who tested positive for drugs rose from 25% in 2007 to 42% in 2016, and marijuana presence doubled in this time frame.4 How this trend will play out in years to come has yet to be seen.

Worsening crash severity – Prior to the impact of the pandemic, the U.S. enjoyed a sustained period of lower fuel prices from 2015 to 2020, resulting in a significant spike in vehicle miles traveled (VMT). Obviously, more miles traveled meant an increase in frequency and severity. At the same time, medical costs continued their upward trends, as did the costs associated with auto liability and uninsured/underinsured motorists claims.

A recent and troubling trend has been a marked increase in the severity of crashes on the nation’s highways. As the coronavirus pandemic impacted business activity during 2020, VMT declined abruptly. However, fatalities per VMT increased by more than 23% year on year. Overall, motor vehicle fatalities rose 5%. Possible reasons? According to the U.S. Federal Highway Administration and the National Safety Council, less congestion tended to prompt faster driving, especially by less risk-averse drivers. In addition, fewer personal automobiles on the road for several months meant that traffic was dominated by larger, heavier trucks, which tend to experience greater effects when involved in crashes. Changing pedestrian patterns may even have contributed to the statistics, as less congested roads yet higher vehicle speeds led to more deadly encounters.5

Rising repair costs – Gone are the days of simply replacing a fender after a collision and marking the claim closed. The increased use of electronics, from onboard computer technology to multiple sensors for collision avoidance, automatic braking, and parking assistance, has radically altered the complexity and costs of auto physical damage claims. A report in Car & Driver magazine6 found that 40% of the value of a new car purchased in 2020 was accounted for in sophisticated, onboard electronics. We’re not just replacing a bumper anymore. We are replacing high-cost hardware, such as cameras and sensors, as well as paying increased labor costs for skilled technicians to install and recalibrate those items into the vehicle’s onboard control environment.

Skilled driver shortage – A demographic change has been impacting many clients with transportation exposures in recent years and is likely to intensify in the years ahead. According to one study, 57% of today’s experienced drivers are over age 45, while 23% are over age 55.7 Younger drivers are not entering the workforce in numbers sufficient to meet demand. Companies will be faced with the duality of either dramatically increasing payrolls to outbid competitors or hiring younger, less experienced drivers. This trend will bear closer examination on renewals, i.e., whether there will be a measurable deterioration in accident frequency and severity due to a cohort of younger, less experienced drivers.

Social inflation/litigation – Litigation is increasingly impacting customers with transportation exposures. While the claims costs of fatalities involving trucking had remained relatively stable until 2014, around 2015 personal injury attorneys began to get much better at going after transportation accounts. One study indicated that the average verdict size for lawsuits above $1 million involving a truck crash increased nearly 1,000% from 2010 to 2018, rising from $2.3 million to $22.3 million.8

Increasing litigation is not only affecting long-haul, for-hire trucking. Grocery operations, retail stores and other clients have trucking and warehouse operations that may have transportation exposures. Also consider the surge in home deliveries that reached new heights during the pandemic, a trend likely to continue well beyond the time COVID-19 is in the rearview mirror.

Customer actions can make a difference

We understand and empathize with rate fatigue in the minds of many customers. Zurich is working hard to provide innovations, risk insights and Risk Engineering services that can help customers exercise greater control over their risk experience, including the management of their Auto exposures. We are committed to working with customers and their brokers in developing alternatives and ideas that can help them manage the impact of rising Auto rates.

Mitigation efforts are always important in seeking greater control over a customer’s total cost of risk. However, the reality of the moment is that the trends discussed above are presently outweighing the best efforts of insurers, brokers and customers. A decade-long period of unprofitability in any line of insurance – indeed for any product or service delivered by a commercial enterprise in any industry – is simply unsustainable. While the hope is that the tempo of rate increases will begin to moderate, trends driving Auto rates are not likely to reverse anytime soon. Distracted driving due to smartphones and legal cannabis will continue to be complicating factors, automobiles will become more costly to repair, medical costs are not trending downward in the foreseeable future, and the litigation industrial complex will continue to flex its collective muscles. Unless and until meaningful change impacts at least some of these trends, the current risk environment in Commercial Auto is almost certain to continue.

More than ever before, transparency on both sides of the insurer/customer relationship will continue to be an important value in weathering a period of increasing rates in Commercial Auto. Keep your broker informed about any changes in your risk profile early in your renewal period to give underwriters time to support the renewal process on a timely basis. And the more data the better, because data drives analytics that can help your company understand and improve your risk profile, which can impact what you pay for coverage.

These are challenging times both for Commercial Auto customers and the carriers providing this important coverage. Working together, we can better understand the trends that are driving results and rates so that we can help customers exercise more effective control over total cost of risk.

1. Commercial Automobile Insurance: Medicine for an Ailing Patient. Conning, Inc. November 2020.

2. Insurance Institute for Highway Safety, Highway Loss Data Institute. Distracted Driving. Cellphone Use and Crash Risk. 2021

3. “Crash rates jump in wake of marijuana legalization, new studies show.” Insurance Institute for Highway Safety, Highway Loss Data Institute. 17 June 2021.

4. Presence of Drugs in Drivers. U.S. Department of Transportation. National Highway Traffic Safety Administration.

5. United States. Federal Highway Administration National Safety Council. Traffic Volume Trends. September 2020.

6. Tingwall, Eric. “Electronics Account for 40 Percent of the Cost of a New Car.” Car and Driver. 2 May 2020.

7. “What’s Driving the Truck Driver Shortage in 2021? Infographic of 6 Key Challenges.” Coyte – A UPS Company. 2021.

8. Brewer, Contessa; Young, Katie. “Rise in ‘nuclear verdicts’ in lawsuits threatens trucking industry.” CNBC. 24 March 2021.

The information in this publication was compiled from sources believed to be reliable for informational purposes only. All sample policies and procedures herein should serve as a guideline, which you can use to create your own policies and procedures. We trust that you will customize these samples to reflect your own operations and believe that these samples may serve as a helpful platform for this endeavor. Any and all information contained herein is not intended to constitute advice (particularly not legal advice). Accordingly, persons requiring advice should consult independent advisors when developing programs and policies. We do not guarantee the accuracy of this information or any results and further assume no liability in connection with this publication and sample policies and procedures, including any information, methods or safety suggestions contained herein. We undertake no obligation to publicly update or revise any of this information, whether to reflect new information, future developments, events or circumstances or otherwise. Moreover, Zurich reminds you that this cannot be assumed to contain every acceptable safety and compliance procedure or that additional procedures might not be appropriate under the circumstances. The subject matter of this publication is not tied to any specific insurance product nor will adopting these policies and procedures ensure coverage under any insurance policy.